Suncor (SU) is the largest Canadian oil company, but not quite large enough to be included with the Big Seven Sisters. (The phrase was coined in the 1950s, referring to the largest seven global oil companies of the time. The original group comprised Anglo-Persian Oil Company (now BP); Gulf Oil, Standard Oil of California (SoCal), Texaco (now Chevron); Royal Dutch Shell; Standard Oil of New Jersey (Esso) and Standard Oil Company of New York (Socony) (now ExxonMobil)).

During the obligatory disclosure period at the end of each quarter, Berkshire Hathaway (BRK.B) revealed it initialed a position in SU by purchasing 17.7 million shares. While still rather minor at just 1.2% of SU shares outstanding, the investment of $500 million is no small potatoes, even for Mr. Buffet. Shares are up nicely to $41 from a purchase price of between $27 and $32.

Suncor is an investment that is depended on its 100-yr potential of oil reserves locked in the Oil Sands. While the firm also produces oil from conventional offshore drilling along the Canadian East Coast and in the North Sea, the majority of its production will come from oil sands.

SU had a rough 2nd quarter 2014 with write-downs of some of its projects. The company wrote down $223 million in Oil Sands projects following a review of certain assets that no longer fit Suncor’s revised growth strategies. SU also incurred $297 million charge against the company’s Libyan assets due to continued political unrest.

The company said production volumes from the Oil Sands operations increased to an average of 378,800 barrels per day in 2Q14—compared to 276,600 bpd in the same quarter last year.

Quarterly production volumes for the Exploration and Production segment decreased to 115,300 barrels of oil equivalent per day (or boe/d). Production volumes were 190,700 boe/d in the same quarter last year, but included conventional natural gas assets recently sold.

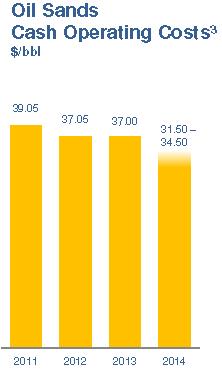

Suncor’s cash cost of production is around $12 per boe offshore in the Maritimes, $6 in the North Sea, and $32 in the oil sands. While operating costs are higher, the future of the company is based on achieving higher production volumes from their sands projects.

The investment trade off with Suncor is accepting higher operating costs in exchange for higher production reserves. SU owns 37 yr. Proven and Probable Reserves compared to 19.7 yrs. for Apache (APA) and 13.5 yrs. for Total (TOT). The amount of estimated recoverable oil in the area of SU’s assets could contain as much as 22.5 billion barrels, which could sustain 500,000-boe production for over 100 years. Below are two graphs from Suncor’s investor presentation outlining planned production growth and historic operating costs from their oil sand projects:

Since 2011, SU has generated $8.3 billion in free cash flow, or operating cash flow less capital expenditures. An important consideration in the oil business is the high cost of capital expenditures needed to offset production declines. Apache generated $0.5 billion in free cash flow and Total $4.1 billion during the same period.

Management has earned a 12-month return on invested capital of 7.75%, and is about the industry average of 8.76%. Operating margins of 16.1% are above industry average of 10.2%.

Suncor pays a dividend of $1.03 a share and offers a 2.5% yield. The dividend was recently raised by 22% and marks the 12 straight year of dividend increases. With a payout ratio of 30%, future dividend increases should track long-term earnings growth rate of 8%.

More information can be found in the most recent Suncor investor presentation:

http://www.suncor.com/pdf/SU_IR_Q2_2014.pdf

First published in the Sept 2014 issue Guiding Mast Investments newsletter, Thanks for reading, George C. Fisher